I know there has been a lot of Safestyle news on DGB in the past few weeks, and for good reason. But since the commercial deal struck with the owner of SafeGlaze announced on Monday, the response to Safestyle from investors has been remarkable. Something we could not have predicted just a few short months ago.

Share price rockets

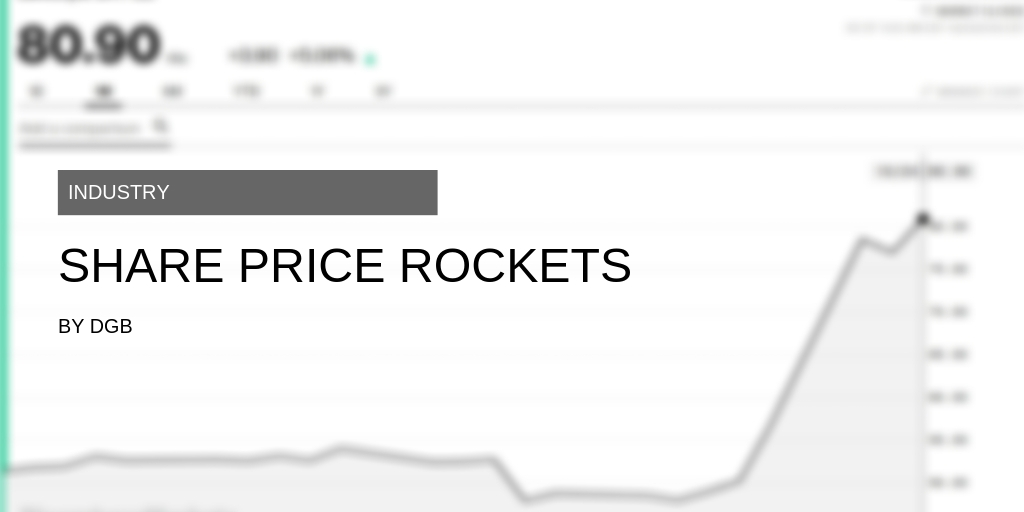

Take a look at this chart:

Credit: Bloomberg

This was a snap shot taken at the end of play yesterday. A decent rise of 5%. But look at that mountain of a line upwards. That represents a near 70% rise from a sub-50p low to over 80p per share now. There was a big initial rise when the deal was announced on Monday, but investors have kept piling into this good news throughout the week.

Investors may be looking at the company, seeing their involvement with the previous owner who managed to build Safestyle up to what it was before the buyout a few years ago, and deciding that and major external risks to the business from competition have disappeared.

If so, yes they have a point. There is a 5 year non-competition clause with the commercial agreement to ensure Mr Misra doesn’t go and start a rival company. But, before everyone gets carried away and think the problems have gone away, we need to look at the wider picture.

One of many problems solved

We have to see this in the wider context. The share price remains just a quarter of what it once was. The decline was rapid, sustained and with just cause. Profit warnings were being issued before SafeGlaze became a competitor. The reasons behind those warnings remain.

Safestyle has to have a business model that suits a 2019 consumer. It is well known now that home owners are more than wise to the variety of sales methods that are designed to get an instant decision under pressure by the sales person. They’re more likely to be kicked out than win an order. Social change has been rapid in the past few years. How long before we see complaints of high pressure selling go viral? If cats with bread around their heads can, this can.

Profit margins have to be rebuilt. That also means a change in product portfolio. There’s little margin left in the “value” part of the market where companies rely on volume to help make money. The companies making good margins and growing well are those who recognised a while ago that quality, higher end products were the way to go. That doesn’t mean ditching shiny White PVCu, because even there you can have a high quality option versus a low quality one. But with prices rising rapidly across the board, the margins on low end work are paper thin as they are.

Market share has to be clawed back. There’s no getting away from the fact that the company lost a fair bit of market share in the past couple of years. The good news from Safestyle’s point of view is that one of their strongly growing competition has now been taken out of the market place. The second bit of good news is that their main national competitors aren’t doing great either. One of which I am going to do a feature on next week. So, if they can manage to get all their ducks in a row, where their competitors currently have not, they might be able to start clawing back some of that lost ground.

What we are seeing here is the share price reaction to the solving of one of various problems. So, it is conceivable that as the above problems are ticked off in the future, we could see the market price of Safestyle start to return to some relative strength.

Still, this was probably was one of the easier issues to solve. Changing ingrained selling methods, changing the business model of what is still a big company, winning back more market share, improving product offerings, are all longer term, arguably harder squares to circle.

To get weekly updates from DGB sent to your inbox, enter your email address in the space below to subscribe:

By subscribing you agree to DGB sending you weekly email updates with all published content on this website, as well as any major updates to the services being run on DGB. Your data is never passed on to third parties or used by external advertising companies. Your data is protected and stored on secure servers run by Fivenines UK Ltd.

{kind=link}

{kind=link}

{kind=link}

{kind=link}